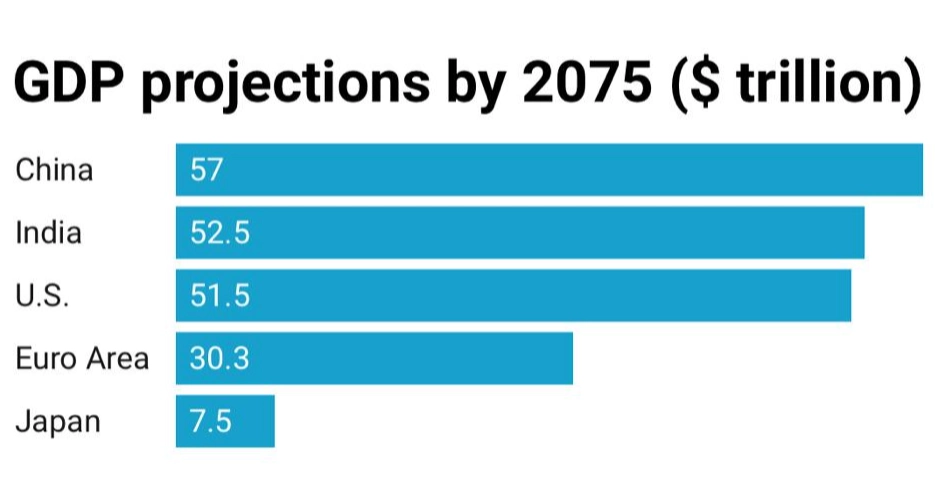

India is on track to become the world's second-largest economy by 2075, surpassing not just Japan and Germany, but even the United States, according to Goldman Sachs.

India now has the world's fifth-largest economy, after Germany, Japan, China, and the United States, reports CNBC.

Also read: Bangladesh now world's 35th largest economy: Canadian publication

Aside from a growing population, the projection is driven by the country's growth in innovation and technology, increased capital investment, and improved worker productivity, according to a recent analysis by the investment bank, it said.

“Over the next two decades, the dependency ratio of India will be one of the lowest among regional economies,” said Goldman Sachs Research’s India economist, Santanu Sengupta.

The dependency ratio of a country is calculated by dividing the number of dependents by the total working-age population. A low dependence ratio shows that there are a greater number of working-age individuals who can support the youth and elderly.

Aslo read: By 2030, Bangladesh will be the 24th largest economy. Here's how ICT is driving that growth

Sengupta went on to say that the key to unlocking the potential of India's fast rising population is to increase labour force participation. And, according to Sengupta, India will have one of the lowest dependence rates among global countries over the next 20 years.

“So that really is the window for India to get it right in terms of setting up manufacturing capacity, continuing to grow services, continuing the growth of infrastructure,” he said.

The Indian government has prioritised infrastructure development, particularly the construction of roads and railroads. The country's new budget plans to maintain the 50-year interest-free lending programmes to state governments in order to stimulate infrastructure investment, the report also said.

According to Goldman Sachs, this is an ideal time for the private sector to ramp up capacity creation in manufacturing and services in order to create more employment and absorb the big labour force.

Also read: Bangladesh to become 25th largest economy in 2034: CEBR

Tech and Investments

According to Goldman Sachs, India's economic trajectory is being driven by advances in technology and innovation.

According to Nasscom, a nonprofit trade organisation, India's technology sector income is predicted to expand by $245 billion by the end of 2023. According to Nasscom's research, this increase will come from the IT, business process management, and software product streams.

Furthermore, Goldman forecasted that capital investment will be a big engine of India's growth, added the report.

“India’s savings rate is likely to increase with falling dependency ratios, rising incomes, and deeper financial sector development, which is likely to make the pool of capital available to drive further investment,” the report stated.